Is a longer-term, lower monthly payment loan saving you money?

Probably not.

Lower monthly payments of longer-term loans often come with higher interest rates, which means you end up paying more money over the life of your loan.

When it comes to borrowing money, it’s wise to consider the total cost of your loan.

If you can afford a higher monthly payment, accepting a shorter-term loan could save you thousands of dollars.

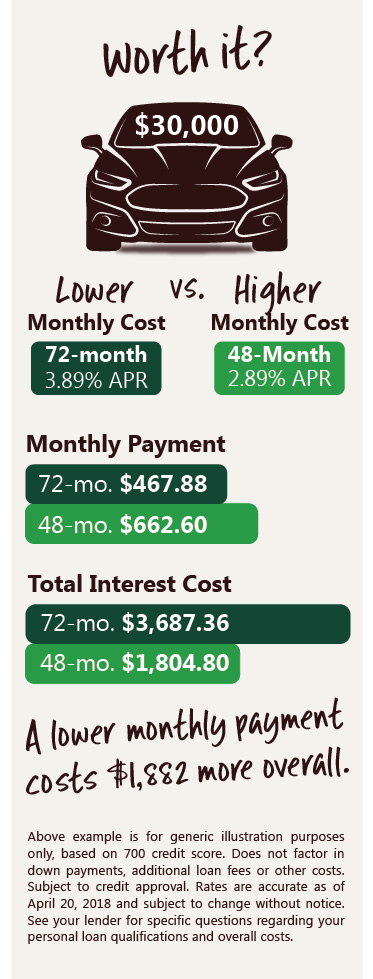

Let’s crunch the numbers on a 48-month (4 year) and 72-month (6 year) auto loan with example an example rate of 2.89% annual percentage rate (APR) for 48 months and 3.89% APR for 72 months for qualified buyers. Rates are for illustration purposes only; See a lender for current rates.

Let’s crunch the numbers on a 48-month (4 year) and 72-month (6 year) auto loan with example an example rate of 2.89% annual percentage rate (APR) for 48 months and 3.89% APR for 72 months for qualified buyers. Rates are for illustration purposes only; See a lender for current rates.

On a $30,000 new car loan, total interest increases from $1,805 for a 48-month term to $3,687 for a 72-month term – a significant cost difference of $1,882.

Focusing on the total loan cost will help you avoid buying more car than you can afford, plus help you avoid owing more on your car than what it is worth.

The longer the financing term, the more susceptible you are to having negative equity and being upside down on your loan.

A typical new car can lose close to 22-percent of its value in the first year, and roughly 12-percent annually in years two through four, according to data from the online car-pricing company Edmumds.com.

If you do go with longer financing, consider buying Guaranteed Asset Protection (GAP) coverage to help mitigate the risk of negative equity and having to make additional principal payments after a total loss. Having GAP can help with the difference between the primary insurance settlement and the outstanding balance on your vehicle on the date of loss. Ask your lender for details.

Get$Fit Tip: Before car shopping, get pre-qualified for financing so you know your numbers. Then, stick to your budget.

Our lenders are happy to answer your questions, even if you are not an RCB Bank customer. Connect with a lender in your area.