When RCB Bank opened its doors for the first time in 1936, we made a promise to Claremore to be friendly in service and progressive in spirit. That promise still directs our decisions today.

“In these ever-changing times, RCB Bank strives to stay true to our roots and provide services that our customers want and need,” said Matt Mason, Claremore market president.

Our progressive spirit continually seeks to develop and deliver flexible and convenient banking options so you can bank how you want, when you want.

We are proud to announce our newest convenience, RCB instaBank, with self-service interactive teller machines, known as ITMs.

Make cash and check deposits for both personal and business. Withdraw cash and coins. Talk with live bankers during extended banking hours.

“The ITM has been a life saver,” said Betty Watowich, owner of Doe’s Eat Place of Claremore. “We don’t carry a bunch of cash so it’s super convenient when we need cash in a flash.”

You can skip the line in the branch or drive-thru and still speak with a teller. At an ITM, you can video chat with a live RCB Bank teller during extended banking hours: Monday – Friday, 7:30 a.m. to 7 p.m. and Saturday, 10 a.m. to 3 p.m., excluding holidays.

“Our video bankers can also help with issues like misplacing a debit card, closing a card and ordering a new one,” said Amber Holloway, branch automation supervisor, RCB Bank. “When you need to talk to a teller but the bank is closed or you’re in a rush, ITMs are a great alternative.”

Non-customers can use our ITMs as well, to cash RCB Bank checks and withdraw funds with their debit card like a normal ATM.

Our friendly service extends beyond our walls. As a locally owned bank, our foundation, our leadership and our drive focuses on community.

“In addition to our financial contributions, you’ll find us in the community, volunteering on local non-profit boards, event committees and at our local schools,” said Sara Moss, community and customer relations, RCB Bank. “We serve because we live here too! Our kids attend these schools too! We serve because we care!“

RCB Bank was formed out of a need during the Great Depression. Good people were struggling. They needed a hand and banks were not meeting their needs. RCB Bank founders stepped in to help local citizens keep their farms afloat and their businesses operating. They made bold moves to lend money because they knew a person’s character, not just their account balance, was worth investing in.

Because of our progressive spirit to loan in tough times, we have had the honor over the years to build loyal customers and serve the needs of multi-generation families.

It is an honor when our customers give us feedback like one of our recent Google Reviews, “Always been there for me!” – Five stars!

RCB Bank is about relationships, community and boldness. We believe building relationships with our customers will help us to better understand and serve their needs. We believe in building stronger communities by providing financial services to help citizens thrive and local businesses grow. We are willing to take bold steps and meet the needs of the community, even in tough times.

We invite you to come and see why so many customers say, RCB Bank “That’s my bank.”

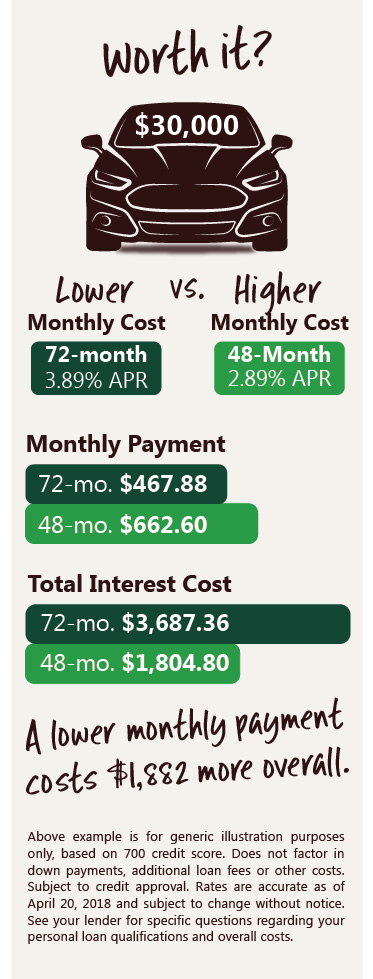

Let’s crunch the numbers on a 48-month (4 year) and 72-month (6 year) auto loan with example an example rate of 2.89% annual percentage rate (APR) for 48 months and 3.89% APR for 72 months for qualified buyers. Rates are for illustration purposes only; See a lender for current rates.

Let’s crunch the numbers on a 48-month (4 year) and 72-month (6 year) auto loan with example an example rate of 2.89% annual percentage rate (APR) for 48 months and 3.89% APR for 72 months for qualified buyers. Rates are for illustration purposes only; See a lender for current rates.